Freelancer Financial Tips

Plan and prep so you can focus on your passions

As a freelancer, the excitement of working on something you love and being your own boss comes with some challenges. You don’t have some of the traditional perks you get from a 9-5. Paychecks come in at varying rates, personal and business budgets, getting your own benefits- it can be a lot to manage.

Not to fear. Here are five tips that may help you live out your passions, while still keeping the financial part of your life in check.

Money Management Tips for Freelancers

1) Know your break even number

This is the number you need to make every month to ensure you can cover your core expenses. Start by filling out a monthly budget with the expenses you will have no matter what – the total of those is your break even number.

Ensuring you have this amount coming in every month can be tricky when contract payments may come in lump sums over time. This is where your emergency fund can come in (see #3), or you might consider a side-hustle job to help you make sure you can cover your monthly expenses.

2) Keep biz and personal expenses separate

It can feel easier to manage all money together, but keeping your personal budget separate from your business budget will benefit you in the long-run and help you avoid financial angst.

Options for doing this range from creating separate accounts to manually categorizing expenses in a spreadsheet at the end of each month. It will make your life simpler come April 15, if your records clearly show personal and business expenses separately.

3) Start building your emergency fund

This is the savings you draw from when an emergency occurs like not receiving a paycheck for a month, or your brakes go out on your car. Emergency funds are critical, especially when your income is unpredictable.

A general rule of thumb would be to save your break even number times six. However, start wherever you can. Be okay dipping into your emergency fund/savings in the short-term to cover personal or business expenses, but know the number your savings cannot go below (i.e. once it hits $xxx, no more pulling from savings).

4) Replicate your corporate benefits as appropriate

As a freelancer, you don’t have access to company sponsored benefits. Start by making sure you have federally mandated major medical health insurance as a baseline. From there, when your budget allows, consider adding other benefits like disability insurance.

Disability insurance covers portions of your income for a fixed amount of time if you become totally disabled due to sickness or injury and cannot work. This coverage could save you a lot of stress should something happen.

Once you feel your business is steady, finances are under control, and you have a reasonable emergency fund consider building retirement savings.

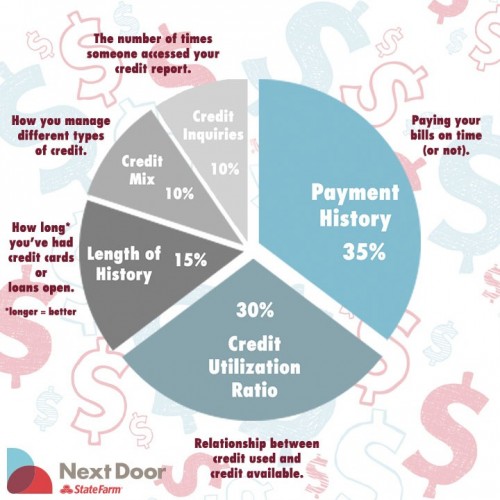

5) Don’t neglect your credit

It may be easy to cover monthly short comings with credit cards or to buy a new computer. However, you want to make sure you’re managing your credit well. Knowing the five factors impacting credit is a good start.

First and foremost, make sure your minimum credit card payment is on time every month. Putting reasonable expenses that you can pay off every month is a good thing for your credit. Secondarily, be aware the higher percentage of your available credit you use, the worse it is for your credit. Try and keep your credit utilization below 30%. For example, if you have a card with a $5000 maximum, keep your balance to $1500 or less.

Building your brand and business as a freelancer is a great opportunity. Follow these tips so your finances are one less thing you have to worry about so you can focus on success.

Next Door®, inspired by State Farm® provides free one-on-one financial coaching, community classes and events, and conference room space in Chicago, IL.

{kind=link}

{kind=link}

{kind=link}

Media Contact

|

Next Door® Financial Coach John www.nextdoorchicago.com |